U.S. Stock Market Volatility (Mid–Late April 2025) An Analytical Overview

Kylo B

4/30/20253 min read

U.S. Stock Market Volatility (Mid–Late April 2025) An Analytical Overview

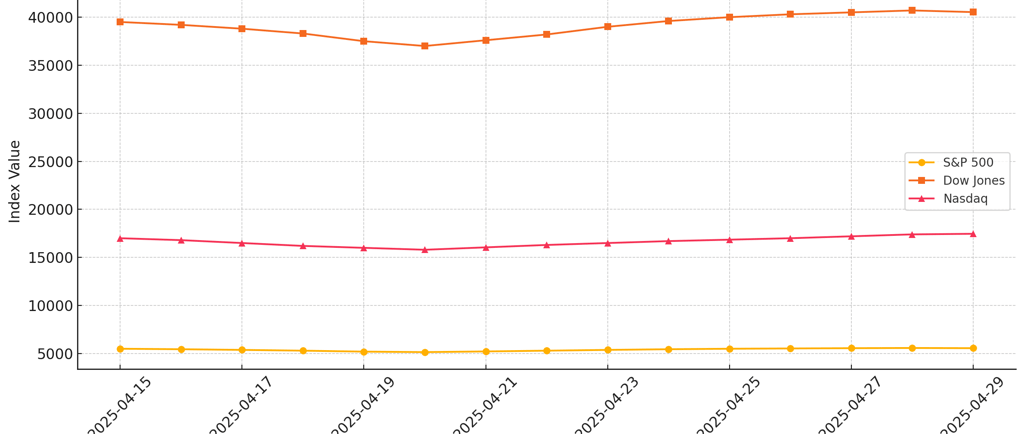

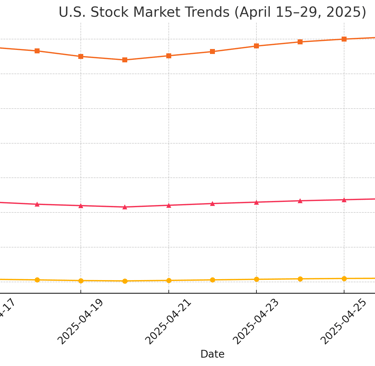

Over the last 10 to 15 days, U.S. financial markets have undergone notable shifts, reflecting a convergence of domestic policy changes, corporate earnings results, and global economic signals. This period has been marked by both sharp declines and recoveries in key indices, including the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average.

Market Performance Summary

April 15–17: Markets experienced a steep decline, triggered primarily by the announcement of new import tariffs by the U.S. administration. These tariffs, affecting a wide array of goods, introduced immediate uncertainty.

April 18–25: After the initial shock, equity markets began a gradual recovery, supported by a strong corporate earnings season and stabilizing investor sentiment.

April 26–29: All major indices posted gains, with the S&P 500 climbing back above 5,560 and the Dow approaching all-time highs near 40,500.

Key Drivers Behind the Market Movement

1. Trade Policy and Tariff Implications

On April 2, the administration announced a new round of tariffs as part of a broader “economic independence” agenda. While aimed at reshoring production and curbing trade deficits, these tariffs sparked immediate concerns:

Business Input Costs: Many U.S. companies rely on foreign raw materials and intermediate goods. Tariffs raised cost projections, especially in manufacturing and tech sectors.

Global Supply Chains: International retaliation (e.g., China imposing reciprocal tariffs) introduced the risk of a renewed trade war, unsettling markets.

Policy Uncertainty: Investors prefer predictability. Sudden announcements without gradual rollouts or clear timelines can heighten volatility.

2. Corporate Earnings Season

Despite the external turbulence, Q1 earnings reports (released mid-to-late April) provided a stabilizing force:

Positive Surprises: Companies like UPS, JetBlue, and General Motors reported better-than-expected earnings, bolstered by improved operational efficiency and robust consumer demand.

Tech Resilience: Major tech firms, while sensitive to global supply costs, showed resilience through innovation and cloud service growth.

Banking Sector: Financial institutions benefited from higher interest rates but expressed caution regarding consumer loan delinquencies, signaling possible economic softening ahead.

3. Consumer and Investor Sentiment

Sentiment Indicators: Surveys from the American Association of Individual Investors (AAII) showed pessimism at levels not seen since the early 1990s, often a contrarian indicator suggesting a market bottom.

Retail Investors: Retail participation dipped early in the period but rebounded slightly as markets recovered.

Flight to Safety: Early in the downturn, there was increased activity in U.S. Treasury bonds, gold, and defensive stocks (utilities, healthcare).

4. Macroeconomic Data Releases

Inflation: Core inflation remained sticky around 3.1%, still above the Federal Reserve’s 2% target. This complicates the case for interest rate cuts.

Labor Market: Jobless claims remained relatively steady, suggesting ongoing strength in employment, albeit with some cooling in hiring across tech and real estate.

GDP Growth: Preliminary Q1 GDP came in at 1.8% annualized—lower than expected, but not recessionary.

Broader Context and Risks

Geopolitical Considerations

Tensions in the Taiwan Strait and ongoing Middle East instability have added to global risk premiums.

U.S.–China economic relations are strained, not only from tariffs but also from ongoing restrictions on tech exports.

Domestic Policy Environment

The Federal Reserve has adopted a wait-and-see stance, holding rates steady while monitoring inflation trends.

Fiscal policy discussions in Congress have added to uncertainty, particularly around budget negotiations and debt ceiling debates.

Forward-Looking Analysis

Markets in the near term are likely to remain sensitive to a few key triggers:

Clarity on Tariff Implementation: If businesses gain clearer timelines and exemption criteria, markets could stabilize further.

Federal Reserve Positioning: Signals of potential rate cuts in the second half of 2025 would likely buoy investor confidence.

Earnings Guidance: While Q1 results were strong, guidance for Q2 and Q3 will be watched closely for signs of slowing growth or inflationary pressures.

The last 10 to 15 days in the U.S. stock market reflect a classic case of volatility amid uncertainty. Policy shifts, both foreign and domestic, exerted pressure, while fundamental earnings strength offered resilience. Investors are navigating a complex environment—where good corporate news is counterbalanced by geopolitical and policy ambiguity. Barring a major external shock, the outlook remains cautiously optimistic, though fragile.